Inventory management is a crucial aspect of any business that deals with physical goods. It involves the planning, tracking, and controlling of the company’s inventory levels to ensure that there is sufficient stock to meet customer demand. While this system has numerous benefits for businesses, there are also some disadvantages to consider. In this article, we will discuss the disadvantages of inventory management.

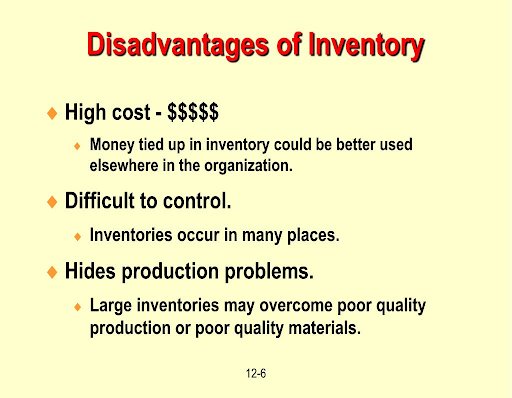

1. High costs

One of the biggest downsides of inventory management is the high cost associated with it. Companies need to invest in specialized software, equipment, and personnel to properly manage their inventory. Additionally, there are costs involved in storing and managing inventory, such as warehouse rental fees, insurance, and utility expenses. This can be a significant burden for small businesses with limited financial resources.

2. Risk of overstocking

Another disadvantage of inventory management is the risk of overstocking. While it’s important to have enough stock to meet customer demand, having excess inventory can tie up company resources and lead to obsolescence. This can happen if the demand for a particular product decreases, or if the company has overestimated customer demand. Overstocking can result in financial loss and negatively impact the company’s profitability.

3. Risk of stockouts

On the other hand, if a company doesn't have enough stock on hand, it may lead to stockouts. This occurs when a customer places an order for a product, but the company does not have enough inventory to fulfill it. Stockouts can lead to customer dissatisfaction and result in lost sales and revenue. It can also damage the company’s reputation, making it difficult to retain existing customers and attract new ones.

4. Time-consuming

Proper inventory management requires a lot of time and effort. Tracking stock levels, placing orders, and updating records manually can be a time-consuming process. This may take away valuable time from other essential business tasks and result in decreased productivity. Small businesses with limited staff may find it challenging to manage their inventory efficiently, leading to errors and delays.

5. Prone to human error

Even with the help of technology, inventory management is still prone to human error. Employees might miscount, misplace, or mishandle products, resulting in inaccurate inventory data. This can lead to issues such as stock discrepancies, stockouts, and overstocking. Human error can be extremely costly and time-consuming to rectify, impacting the company's bottom line.

6. Upfront investment

To implement an effective inventory management system, companies have to make a significant upfront investment. This includes purchasing the necessary software, training employees, and restructuring their operations. For small businesses with limited financial resources, this can be a barrier to adopting inventory management practices.

7. Limited flexibility

Some inventory management systems can be rigid and inflexible, making it challenging to adapt to changes in the business environment. For example, if a new product is introduced or customer demand shifts, the existing inventory management system may not be able to adapt quickly. This can result in stockouts or overstocking, affecting the company's ability to meet customer demand and maintain profitability.

In conclusion, while inventory management is essential for the smooth functioning of a business, it comes with its fair share of disadvantages. The high costs, risk of overstocking and stockouts, time-consuming nature, human error, upfront investment, and limited flexibility are some of the major downsides of inventory management. Companies need to carefully consider these factors when implementing an inventory management system and find ways to mitigate these disadvantages to reap the benefits of proper inventory management.